For many professionals, business owners, and wealth accumulators, building a diversified investment portfolio is a critical step toward long-term security. You may already know the classic investment principle that diversification is the “only free lunch” available, serving as a powerful tool to manage market volatility and protect your financial future.

However, when you look beyond individual shares or property, you are quickly confronted with a confusing alphabet soup of listed investment options on the Australian Securities Exchange (ASX): ETFs, LICs, and LITs.

A common mistake investors make is focusing entirely on what a fund invests in, while overlooking how that fund is structured. Yet, the structure itself can have a meaningful impact on tax outcomes, liquidity, and overall portfolio behaviour.

Understanding these differences is key to making more informed and confident investment decisions. In this article, we take a practical, jargon-free look at the three primary listed investment structures (ETFs vs LICs vs LITs) in Australia, and explain why these structural differences matter.

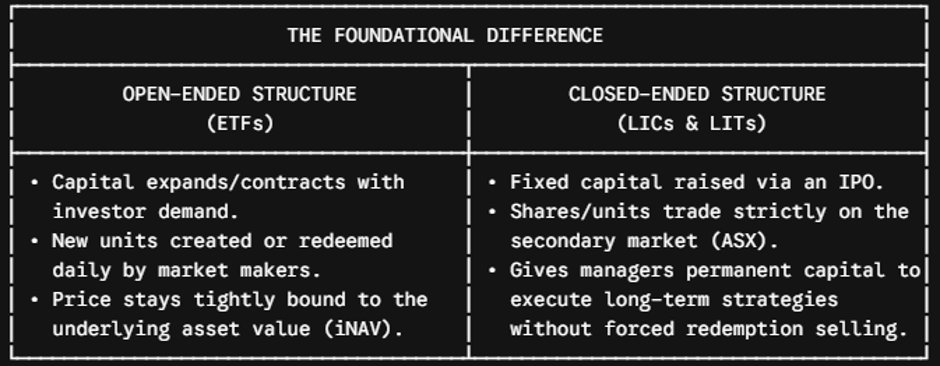

Open-Ended vs Closed-Ended: The Foundational Difference

To understand listed investments, we must first look at how a fund manages its underlying capital pool. Listed structures generally fall into one of two categories: open-ended or closed-ended. This distinction fundamentally shapes how units are priced and how the fund manager operates.

Open-Ended Structures

In an open-ended structure, capital can continuously flow into and out of the fund. When new investors buy into the fund, new units are created; when investors want to exit, units are redeemed directly with the fund registry, and cash flows out. Because the fund expands and contracts based on investor demand, the manager must maintain sufficient liquidity to meet potential redemptions. This can sometimes limit the manager’s ability to hold less liquid, long-term assets.

Closed-Ended Structures

In contrast, a closed-ended structure raises a fixed amount of capital through an Initial Public Offering (IPO). Once listed on the exchange, the fund is effectively “closed”—no new money can be directly added to or withdrawn from the fund registry. If you want to buy or sell shares, you must trade with an existing investor on the secondary market (the ASX) via a broker. This provides the manager with a stable, permanent pool of capital, removing the pressure to sell assets quickly during a market downturn to fund investor redemptions.

Exchange-Traded Funds (ETFs)

Exchange-Traded Funds (ETFs) are the open-ended workhorses of modern investing, having experienced significant growth over the past two decades as vehicles for global diversification.

- The Structure: ETFs are established as open-ended unit trusts.

- Trading Mechanics: They trade on the ASX exactly like regular shares, allowing investors to execute orders through standard online broking accounts.

- Pricing and Liquidity: Unlike traditional unlisted funds, ETFs utilize specialized institutional participants known as “market makers”. These market makers continuously buy and sell units on the exchange, creating or redeeming supply to match investor demand. Because of this mechanism, the trading price of an ETF remains tightly bound to its Indicative Net Asset Value (iNAV). This means you are highly likely to buy or sell your units at a price that accurately reflects the true value of the underlying assets, with minimal premium or discount.

- Management Style: Traditional ETFs are passively managed, meaning they look to replicate the performance of a specific index or benchmark, such as the Australian S&P/ASX 200, the US S&P 500, or global asset classes. However, the market has expanded to include Exchange-Traded Managed Funds (ETMFs), which feature active portfolio management styles.

Listed Investment Companies (LICs)

Listed Investment Companies (LICs) represent some of the oldest investment vehicles in Australia, with the earliest examples listing on the ASX in the 1920s.

- The Structure: A LIC is established as a corporate entity (a company) rather than a trust structure.

- The Closed-End Advantage: Because the underlying capital pool is closed, LIC managers are insulated from short-term redemption pressures. This gives them the flexibility to capture “illiquid premiums” by investing in asset classes that take longer to buy or sell, such as small-cap companies or unlisted opportunities, which can support long-term strategic growth.

- The Premium and Discount Dilemma: Because LIC shares are fixed and trade strictly between buyers and sellers on the open market, the price is heavily driven by market supply and demand. As a result, a LIC’s share price can diverge significantly from its Net Tangible Assets (NTA). If a LIC is highly sought after, it may trade at a premium (paying more than the underlying assets are worth). If market sentiment turns negative, it can trade at a deep discount (buying assets for less than their underlying value).

- Management Style: LICs are predominantly actively managed, with portfolio managers aiming to outperform benchmarks and generate “alpha”.

Listed Investment Trusts (LITs)

Listed Investment Trusts (LITs) sit alongside LICs as long-standing closed-ended options on the ASX, but they feature an entirely different legal and tax framework.

- The Structure: A LIT is structured as a closed-ended trust rather than a company.

- Trading and Pricing: Just like LICs, LITs trade on the exchange and are subject to market demand forces, meaning they can also experience prolonged periods of trading at a premium or a discount to their underlying NTA.

- Asset Focus: Active managers frequently use LITs to grant retail investors access to specialized, income-focused asset classes. These commonly include global fixed income, corporate bonds, and private debt markets. The closed-ended structure is ideal for these assets, as it allows the manager to hold fixed-income instruments securely to maturity without having to liquidate them early to pay out departing unitholders.

Why Structure Matters: Tax Efficiency and Income Flow

When evaluating these structures, the choice often hinges on tax efficiency, income sustainability, and your specific lifecycle stage.

The Corporate Dividend Layer (LICs)

Because a LIC is a company, it is subject to the Australian corporate tax rate (typically 30%) on its investment income and realized capital gains before any money reaches you. However, this structure offers a distinct strategic advantage for income planning: a LIC does not have to distribute all of its earnings immediately. It can retain profits from strong financial years and pass them through during market downturns, creating a smooth, predictable dividend stream. Furthermore, these distributions often come with franking credits attached, which can be highly tax-effective depending on your personal marginal tax rate.

The Trust Pass-Through Layer (ETFs & LITs)

Conversely, both ETFs and LITs operate under a trust framework. Under Australian tax law, a trust cannot retain earnings; it must pass through all dividends, interest, and realized capital gains in full to unitholders each financial year. This income is then taxed directly at your individual marginal tax rate. While this ensures immediate transparency, it means that the fund manager cannot smooth out income payments from year to year, leaving your annual distributions more exposed to underlying market fluctuations.

Risks and Common Strategic Pitfalls

Every investment structure involves distinct trade-offs and structural risks that must be carefully weighted against the benefits:

- Buying the Premium: A frequent investor mistake is purchasing a popular LIC or LIT when it is trading at a significant premium to its NTA. If market enthusiasm cools and the structure reverts to its historical average or a discount, you can experience a capital loss even if the value of the underlying investments remains stable.

- Assuming Constant Liquidity: While ETFs offer reliable, highly liquid trading environments due to active market makers, closed-ended LICs and LITs rely entirely on independent buyers and sellers on the ASX. During broader market sell-offs, lower trading volumes can make it difficult to exit a LIC or LIT quickly without accepting a severe discount.

- Underestimating Ongoing Drag: While passive index-tracking ETFs are generally very low-cost, actively managed LICs and LITs often carry higher base management fees and performance fees. Investors must evaluate whether the manager’s potential to generate alpha justifies the higher structural costs over the long run.

A Practical Scenario: Structuring a Tailored Portfolio

To see how these concepts integrate into real-life strategic planning, let’s look at a typical scenario for a professional family in their wealth accumulation phase.

Consider Sarah and David, a Perth-based couple in their mid-40s. They are focused on long-term strategic investing outside of their superannuation to give them financial options as they approach retirement. They want to optimize tax efficiency, manage portfolio risk, and capture sustainable growth.

Rather than attempting to find a single “best” vehicle—which does not exist—a balanced portfolio approach can strategically combine these structures to align with their specific goals:

- The Core Portfolio (ETFs): They allocate the foundation of their portfolio to low-cost, passive ETFs tracking broad Australian and international equity indexes. This guarantees highly liquid, cost-effective diversification across thousands of global companies.

- The Active Satellites (LICs & LITs): To build on this core, they add a targeted allocation to a long-established LIC with a proven history of generating capital growth and a steady stream of franked dividends, maximizing their tax efficiency. They also select a specialized LIT focused on global private debt to inject a stable, high-yielding income stream that is uncorrelated with traditional share markets.

This structural combination allows them to achieve low overall costs, capture active investment opportunities, and maintain strong risk boundaries.

Side-by-side comparison: ETFs vs LICs vs LITs

| Key Feature | Exchange-Traded Funds (ETFs) | Listed Investment Companies (LICs) | Listed Investment Trusts (LITs) |

| Legal Entity Type | 📜 Unit Trust | 🏢 Public Company | 📜 Unit Trust |

| Capital Pool | 🔄 Open-Ended (Fluctuates based on daily inflows/outflows) | 🔒 Closed-Ended (Fixed pool of capital raised at IPO) | 🔒 Closed-Ended (Fixed pool of capital raised at IPO) |

| Pricing Mechanism | 🎯 Tightly Bound to NAV Kept in check by active market makers. | ⚖️ Market Supply & Demand Can trade at a significant premium or discount to NTA. | ⚖️ Market Supply & Demand Can trade at a significant premium or discount to NTA. |

| Tax Framework | 🔄 Pass-Through Structure Income & capital gains are passed directly to you pre-tax. | 💼 Corporate Structure Pays corporate tax (up to 30%) on income before making payouts. | 🔄 Pass-Through Structure Income & capital gains are passed directly to you pre-tax. |

| Income Distribution | 📊 Lumpy / Direct Must distribute all income annually. Cannot retain earnings to smooth payments. | 🛡️ Smoothed Dividends Can retain profits from good years to maintain regular dividends during downturns. | 📊 Lumpy / Direct Must distribute all income annually. Cannot retain earnings or smooth payments. |

| Franking Credits | 🏷️ Passed Through Attaches whatever franking credits are received from underlying stocks. | 💎 Generated internally Can offer fully franked dividends via the company tax it pays. | 🏷️ Passed Through Attaches whatever franking credits are received from underlying holdings. |

| Primary Style & Assets | 🌐 Passive Index / Broad Market Tracks specific sectors or global indexes (Active options growing). | 📈 Active / Equities Focus Aims to outperform the market (Alpha) via domestic or global shares. | 💵 Active / Specialized Income Often targets private debt, corporate bonds, or alternative assets. |

Key Risks & What Investors Should Watch

- The Premium/Discount Trap: LICs and LITs often trade at persistent discounts to Net Tangible Asset (NTA) value. These discounts can persist for years. There are rarely “dollars selling for eighty cents” in markets, and waiting for these discounts to close can lead to a long and frustrating investment experience. Conversely, purchasing a popular if LIC or LIT at a large premium means paying more than the underlying assets are worth.

- Liquidity Differences: ETFs have deep liquidity via market makers. In contrast, LICs & LITs rely entirely on finding buyers or sellers on the stock exchange, which can prove difficult during severe sell-offs or times of distress.

- Management Fee Drags: While passive index-tracking ETFs are generally low-cost, actively managed LICs, LITs, and Active ETFs (ETMFs) typically charge higher base and performance fees. So you must judge whether the manager’s ability to generate alpha (outperformance) or provide access to specialized assets justifies these higher costs over the long run.

Summary: Key Strategic Takeaways

Navigating listed investment vehicles requires looking past short-term marketing and understanding the operational machinery underneath:

- ETFs provide highly liquid, transparent open-ended access to broader markets close to asset value, making them excellent choices for low-cost core holdings.

- LICs offer a company structure capable of smoothing out income and passing through franking credits, but require careful navigation around premiums and discounts to NTA.

- LITs offer a closed-ended trust framework suited for securing specialized, income-generating alternative asset classes like private debt and fixed income.

Choosing how to blend these structures depends entirely on your cash flow needs, tax positioning, and long-term financial strategy.

If you are looking to strip away the complexity of your investments and build a transparent, evidence-based portfolio tailored to your lifestyle goals, reach out to us at Simplify Financial Planning today.

General Advice Disclaimer

The information contained in this article is general in nature only and has been prepared without taking into account your personal objectives, financial situation, or needs. Before making any investment decision based on this information, you should consider its appropriateness having regard to your circumstances, and consider seeking professional advice from a qualified financial planner.